We are happy to release a new paper on the ePBS free option problem: The Free Option Problem of ePBS.

We extend our previous research posts Part I and Part II on the ePBS free option problem. We describe in more detail the methodology previously used and introduce a new mitigation mechanism, dynamic penalties.

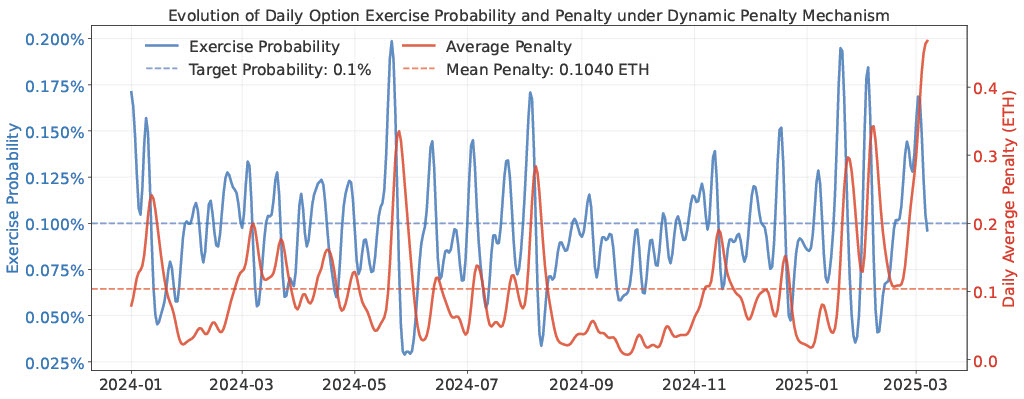

Previously, we observed that shortening the option window and adding penalties can help decrease the option exercise probability and option valuable. However, it comes with trade-offs. Shortening the time window between PTC deadlines directly undermines one of the key benefits of ePBS: scalability. Penalties decrease the option exercise probability, but make building more costly. Ideally, the option would be only exercised on a small fraction of blocks, while keeping penalties small. This is impossible with a static penalty, since market conditions vary continuously. In the paper, we show, however, that under mild conditions, it is possible with very simple adaptive penalties: If the option is exercised in the previous block, you increase the penalty; otherwise, you decrease it.

The mechanism gives strong theoretical guarantees and achieves, in historical block data, an average exercise probability of 0.096\%, well below the no-penalty baseline (0.82%) and comparable to the level under a high static penalty of 0.5 ETH (0.107%) with an average penalty of only 0.104 ETH. Beyond average conditions, the dynamic penalty mechanism also adapts effectively on high-volatility days.

In short, we think that Dynamic penalties can be an effective short-term patch to mitigate the free option problem.