TL;DR

Ahead-of-time allocation mechanisms are often criticized for creating room for just-in-time secondary markets that benefit intermediaries rather than the primary auctioneer. In our latest paper, we test this idea using Arbitrum’s Timeboost auction after its main users switched to the Kairos resale market. Our main finding is that weak competition in the primary auction, potentially amplified by the ahead-of-time design, led its main users to rely on Kairos to retain more value, while Arbitrum captured a smaller share of the value generated around Timeboost. The broader takeaway is that ahead-of-time allocation mechanisms may be especially vulnerable to intermediary markets when competition among dominant participants is weak.

Joint work with @Christoph and @kakia

We thank @thomasa and @BrunoMr from Flashbots and George Davies from Kairos for their valuable feedback on this post and earlier versions of the paper.

The Problem

On blockchains, ordering rights are typically allocated just in time. Whether bidding for the right to build the next block or competing for top-of-block execution, participants can bid immediately before the auction resolves and block contents are finalized. Yet some designs allocate these rights ahead of time. Slot auctions in Ethereum are one prominent example: builders bid before knowing the exact block contents they will eventually submit. Such designs may offer advantages, such as more predictable execution, but they also risk concentrating rights in the hands of a small set of parties with the highest expected value. These parties can then resell those rights just in time, for example when realized opportunities differ from ex ante expectations, allowing them to capture additional revenue.

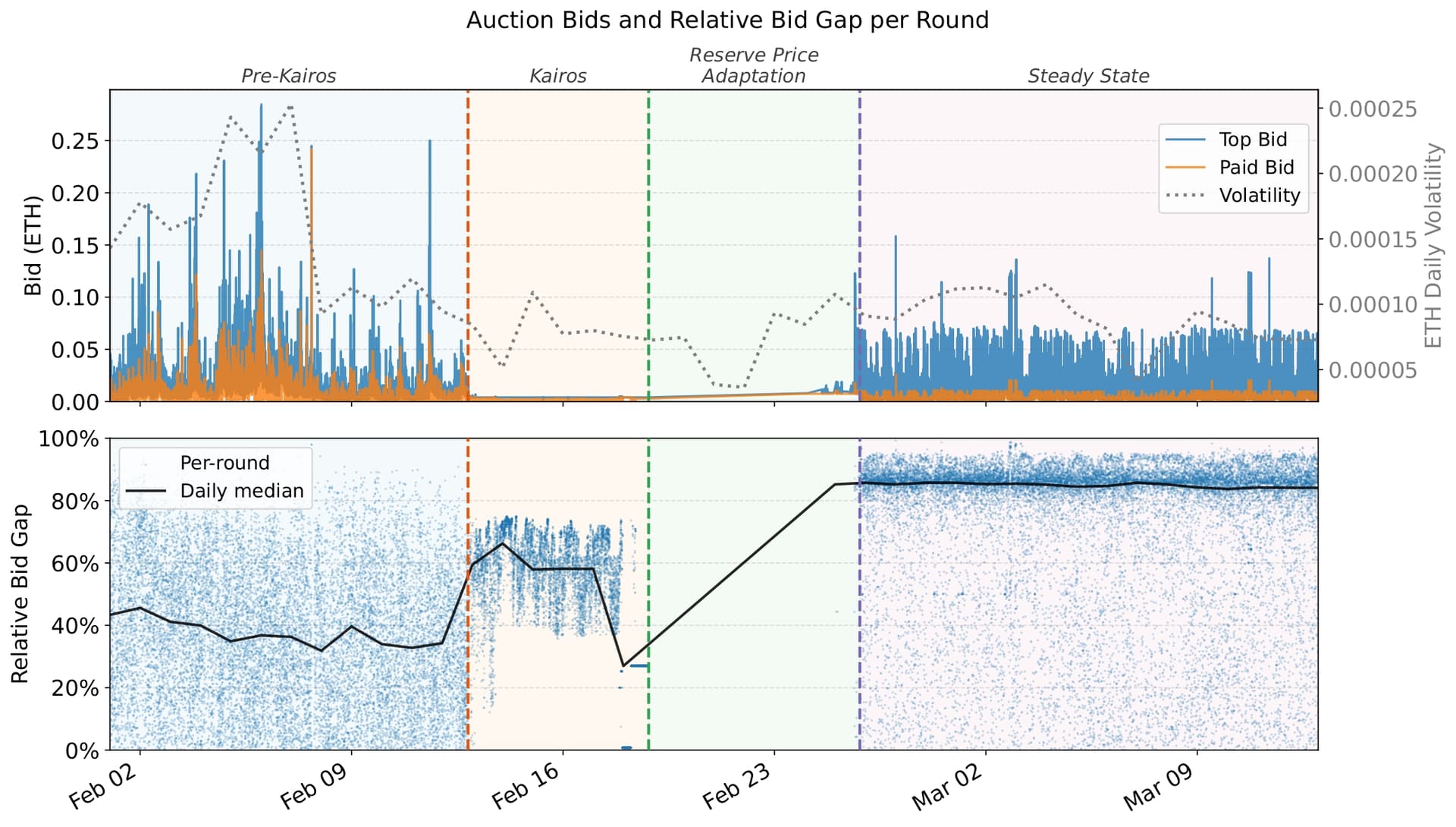

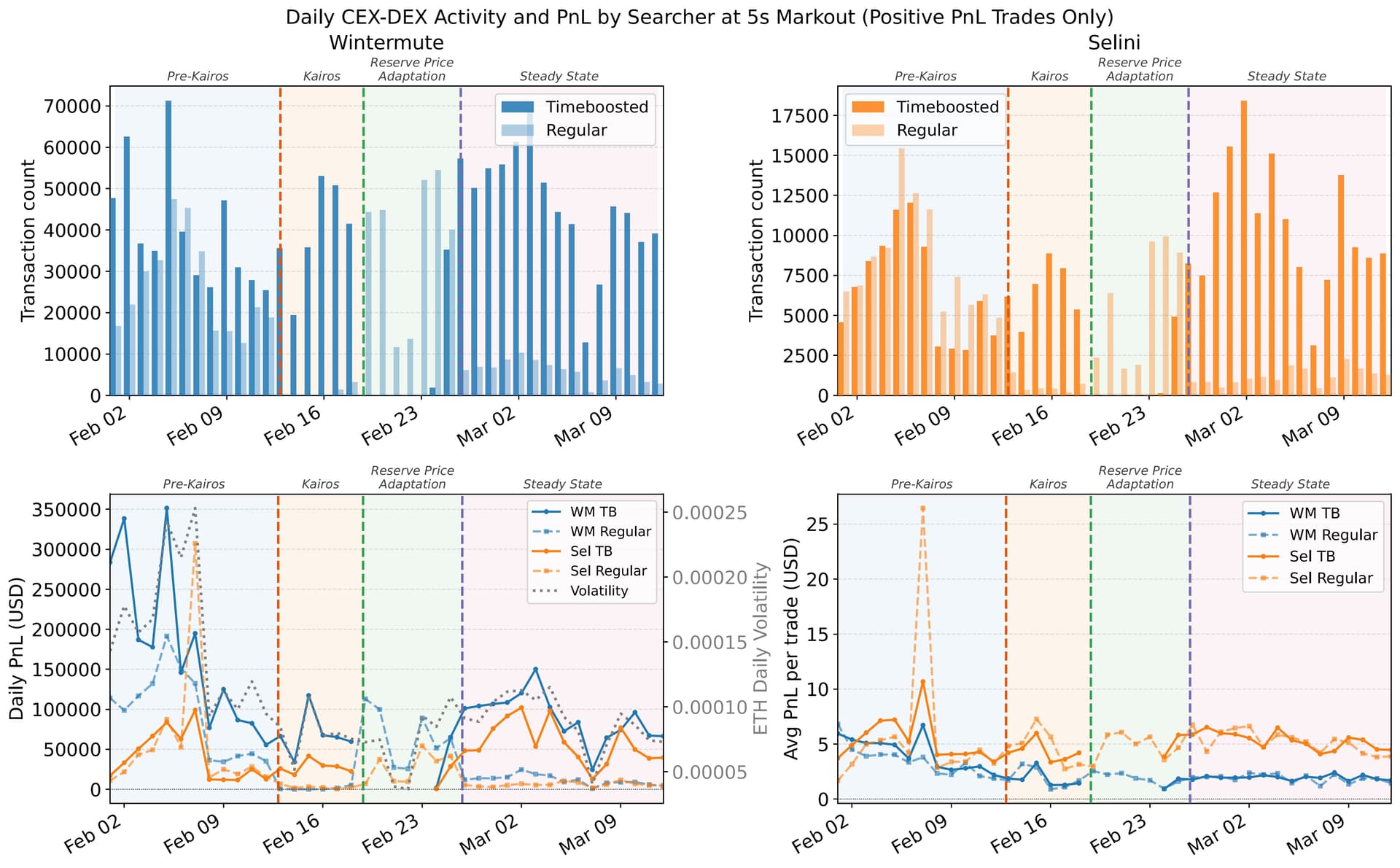

Arbitrum’s Timeboost auction is one such ahead-of-time allocation mechanism (the auction for the next one-minute round starts at second 0 and runs until second 45, with the remaining 15 seconds reserved for on-chain settlement). It sells time-advantaged ordering rights, giving the winner the ability to bypass the sequencer’s default 200ms delay. Until recently, the auction was dominated by two CEX–DEX searchers, Wintermute and Selini. That changed when Kairos, a resale service for fast-lane access, began winning most auctions after these searchers shifted from competing directly in the primary auction to sourcing access through the secondary market.

In our recent paper, we study the implications of this shift in auction dynamics and analyze how the emergence of the Kairos resale market affects competition, value capture, and surplus around Timeboost. While these insights do not map perfectly to every allocation mechanism, the broader lesson is clear: when competition in the primary market is weak, secondary markets can sharply reduce protocol value capture, and the ahead-of-time component may make this worse by limiting entry from participants who are only occasionally competitive.

The Incentives for a Secondary Market

In the context of Timeboost, participants may prefer to bypass direct competition in the primary auction and use a service like Kairos for three main reasons:

- Unbundling: Instead of wholesaling the time advantage for an entire minute, Kairos can reallocate it at a much finer granularity. This can improve efficiency by assigning fast-lane access to whoever values it most at a given moment.

- Weakened competition: Participants in the primary auction may have incentives to bid less aggressively and leak less value to the auctioneer, with Kairos effectively acting as an intermediary in that structure.

- Information: Bidding closer to execution gives participants more information about realized opportunities, which can improve allocation efficiency. Also, the reseller may be able to decide when resale is especially valuable, although we do not observe Kairos behaving this way directly.

These mechanisms imply different empirical patterns. The first and third predict higher total value extraction, while the second mainly predicts a redistribution of value rather than additional value creation. Our results provide the strongest support for the second mechanism, suggesting that weakened competition is the main driver of the observed market dynamics.

| Mechanism | Total Value Extraction | Side Effect |

|---|---|---|

| Unbundling | Higher | Broader searcher set |

| Weakened competition | Similar | Lower auction revenue |

| Information | Higher | Larger spread between primary and secondary markets |

The Transition to Kairos

To test our theoretical predictions and understand how the adoption of Kairos affects competition, value capture, and surplus around Timeboost, we analyze all auction rounds between February 1 and March 12, 2026, together with transaction-level data for Wintermute, Selini, and Kairos. Full methodological details are in the paper. We focus on three key events that shape the market dynamics during this period:

- Feb 12: Wintermute and Selini reduce participation in the primary auction and begin using Kairos

- Feb 18: Arbitrum increases the reserve price from 0.001 to 0.0075 ETH

- Feb 25: Arbitrum restores the reserve price to 0.001 ETH

For convenience, we refer to the resulting periods as Pre-Kairos, Kairos, Reserve Price Adaptation, and Steady State.

Competition in the Primary Auction Collapsed

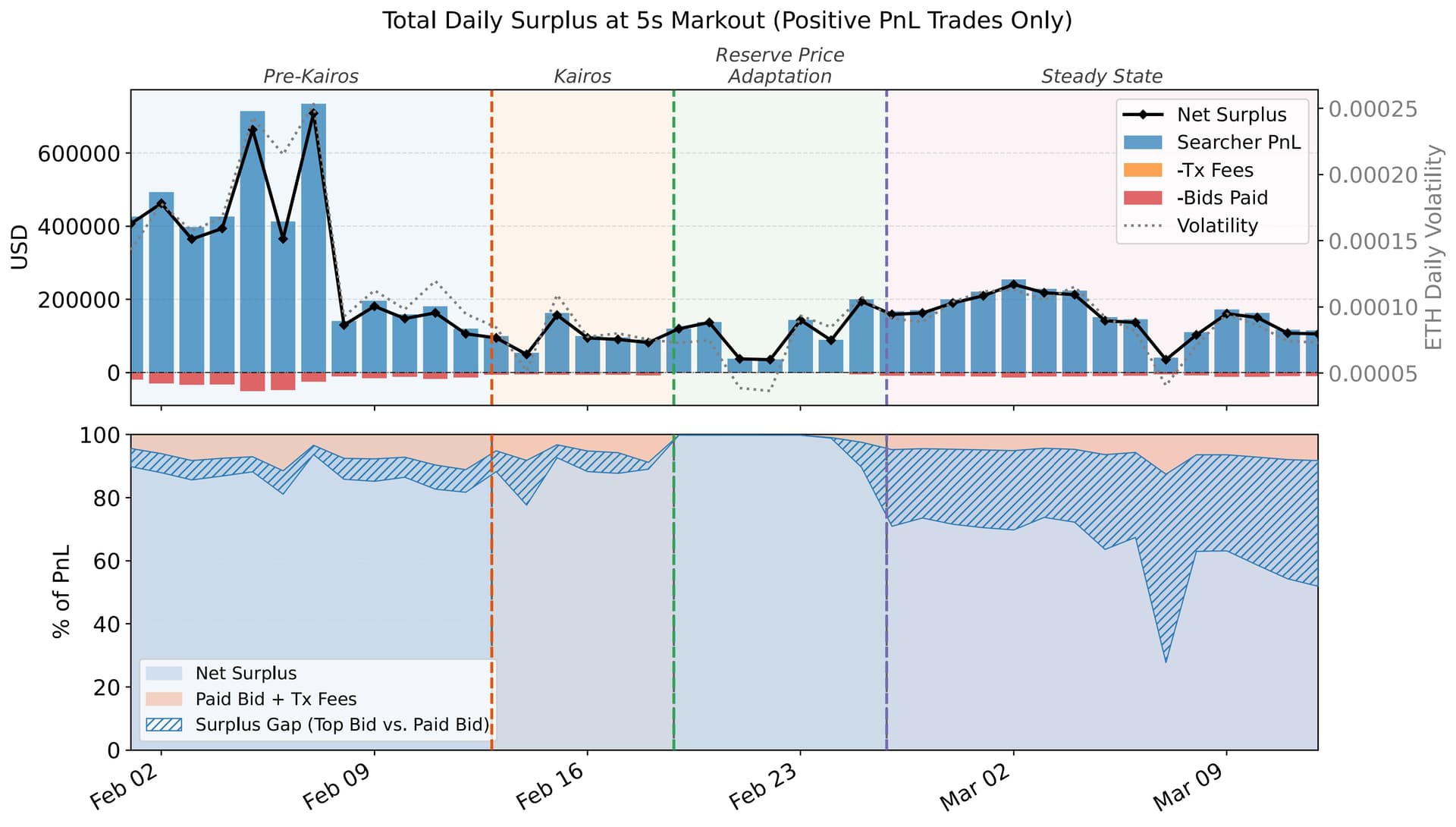

After Wintermute and Selini switched to Kairos, the market settled into a new regime in which Kairos won roughly 75–80% of auction rounds and resold fast-lane access through a secondary market. At first glance, this does not look like a collapse in participation: in the steady state, all three entities still bid in most rounds. But the auction is no longer meaningfully competitive. Before Kairos, Arbitrum captured about 63% of the top bid on average; after the transition, it captured only about 15%. The reason is simple: while Kairos continues to submit competitive bids, Wintermute and Selini bid much lower than before. As a result, the gap between the top bid and the paid bid widens dramatically, and the primary auction captures only a limited share of the value reflected in bids.

Demand for Fast-Lane Access Remained Strong

Importantly, the drop in auction competitiveness did not reflect a disappearance of demand. Before adopting Kairos, Wintermute and Selini used both the fast lane and the regular lane for their CEX–DEX trades. After the switch, they relied almost entirely on the fast lane, using Kairos to access it continuously rather than bidding directly in the primary auction. Time-boosted activity remained high and continued to track price movements closely. In other words, searchers still wanted fast-lane access just as much, but that demand was now routed through the intermediary rather than expressed through competitive bidding in the primary auction.

Arbitrum Captured a Smaller Share of the Value

The shift to Kairos did not meaningfully increase total value extraction. Searcher surplus remained of broadly similar magnitude across regimes, suggesting a redistribution of value rather than an expansion of it. What changed was how much of that value Arbitrum was able to capture. In the pre-Kairos period, stronger competition meant a larger share of surplus was passed through the auction. In the steady state, by contrast, the top bid corresponds to a much larger share of surplus than the paid bid, and the gap between the two widens substantially. So the key change is not that bidding stops responding to valuable opportunities. It is that weaker competition causes a smaller fraction of that value to be captured through the paid bid. The result is a growing disconnect between value creation and auction revenue.

The Broader Lesson for Ahead-of-Time Allocation

Our main takeaway is that the Arbitrum case is at least as much about weak competition as it is about ahead-of-time design. The concentrated searcher market in Timeboost likely made it easier for a secondary market like Kairos to emerge and shift value away from Arbitrum. The ahead-of-time structure may have amplified this by limiting entry from participants who are only occasionally competitive, but the dominant force in our data appears to be the lack of strong competition in the primary market.

This lesson matters beyond Arbitrum. Timeboost is mainly useful for CEX–DEX searchers, so it is not a perfect analogue for all of Ethereum MEV. Still, the broader pattern is relevant: when a small set of dominant participants face limited competition, secondary markets can emerge and reduce protocol value capture. Ethereum’s searcher and builder markets are not yet as concentrated as Arbitrum’s Timeboost market, but both have become more concentrated over time. If competition were to weaken substantially, similar dynamics could plausibly emerge there as well.

There is also an important asymmetry. Arbitrum can respond to these dynamics with tools like aggressive reserve-price adjustments. Ethereum mainnet would likely have fewer such options, especially where they could conflict with broader concerns like liveness. So while Ethereum may currently be better protected by healthier competition, it could also be more exposed if that competition breaks down.

References and Related Work

-

Burak Öz, Christoph Schlegel, and Akaki Mamageishvili. Just-in-Time Resale in an Ahead-of-Time Auction: An Event Study. arXiv preprint arXiv:2603.20175, 2026. [2603.20175] Just-in-Time Resale in an Ahead-of-Time Auction: An Event Study

-

Mallesh Pai and Max Resnick. Centralization in Attester-Proposer Separation. arXiv preprint arXiv:2408.03116, 2024. [2408.03116] Centralization in Attester-Proposer Separation

-

Akaki Mamageishvili, Christoph Schlegel, Ko Sunghun, Jinsuk Park, Ali Taslimi. TimeBoost: Do Ahead-of-Time Auctions Work? arXiv preprint arXiv:2511.18328, 2025. [2511.18328] TimeBoost: Do Ahead-of-Time Auctions Work?